At the moment, there are no entries available for display

Basis of Preparation

1. Reporting entity, organisation boundary and reporting period

The sustainability-related financial disclosures presented in this section apply to Commercial Bank of Ceylon PLC (the Bank), and its Subsidiaries (together referred to as the “Group “and individually as Group entities) within the financial reporting boundary, in line with the Bank’s general purpose financial reports. The disclosures in this section are provided on a consolidated basis, unless otherwise stated.

This report covers the financial year from January 01, 2025 to December 31, 2025, consistent with the Group’s financial reporting period.

2. Application of SLFRS Sustainability Disclosure Standards

This section has been prepared in accordance with the SLFRS Sustainability Disclosure Standards, SLFRS S1 on “General Requirements for Disclosure of Sustainability-related Financial Information” (SLFRS S1), and SLFRS S2 on “Climate-related Disclosures” (SLFRS S2), issued by The Institute of Chartered Accountants of Sri Lanka (adopted based on the IFRS S1 and IFRS S2 issued by The International Sustainability Standards Board).

The disclosures presented here are intended to support primary users of general-purpose financial reports in understanding the climate-related risks and opportunities (CRROs) that could reasonably be expected to affect the Group’s:

- cash flows,

- access to finance or

- cost of capital over the short, medium or long term (Group’s prospects).

3. Value chain

The Bank operates within an interdependent value chain system characterised by dual dynamics; dependencies and impacts as described in the section Business model for sustainable value creation. The Bank relies on multi-capital resources (financial, manufactured, intellectual, human, social & relationship, and natural) across its value chain to derive value. The Bank simultaneously influences these capitals either through value creation, preservation or erosion.

In the assessment of CRROs, the upstream and downstream value chain was considered using all reasonable and supportable information available without undue cost or effort for a comprehensive understanding of the CRROs.

Upstream value chain

Upstream activities, as outlined in the Business model for sustainable value creation, involve the Bank’s engagement with external stakeholders to secure financial and non-financial capital essential for its operations. The Bank derives value from six types of capitals namely, Financial, Manufactured, Intellectual, Human, Social & Relationship, and Natural, which serve as upstream inputs forming the foundation of its business activities. The CRROs impact the Bank’s upstream activities by impacting both internally managed capitals and the Bank’s ability to maintain stable access to financial and non-financial capital from external stakeholders.

Internal operations

Internal operations refer to the Bank’s core functions, processes, systems, and people that transform the six types of input capital into products, services, and strategic outcomes. As shown in Figure 12 – Business model for sustainable value creation, the “Value generating activities” at the center represent these internal processes, which include lending and investment decisions, risk and compliance management, innovation and product development, staff development, IT and infrastructure management, and Environmental, Social and Governance (ESG) integration including climate risk governance. These activities are crucial for creating value from capital inputs and underpin both the Bank’s short-term performance and long-term resilience. The CRROs can impact these internal operations, affecting the Bank’s ability to convert capital into value.

Downstream value chain

Downstream activities encompass the Bank’s outward-facing actions and services that deliver value to stakeholders, including financial product deployment, client engagement, post-disbursement monitoring, and contributions to economic, environmental, and social outcomes as illustrated in the far-right portion of Figure 12 – Business model for sustainable value creation.

Downstream value chain drives external capital formation by reinvesting in the six types of capital such as promoting financial inclusion, enhancing social capital through ethical practices, and supporting green infrastructure. Downstream activities are a critical component of the Bank’s value chain, exposing the Bank to the CRROs through its interactions with borrowers, sectors, and markets, with direct implications for financial performance and long-term value creation. Climate risks may affect borrower resilience and portfolio stability, while also creating opportunities to advance sustainable finance, support low-carbon transitions, and generate positive value for stakeholders and the environment.

4. Basis of materiality

SLFRS S1 describes the requirement to disclose material information about the Sustainability-related Risks and Opportunities (SRROs) that could reasonably be expected to affect the entity’s prospects. In the context of sustainability-related financial disclosures, information is material if omitting, misstating or obscuring that information could reasonably be expected to influence decisions that primary users of general-purpose financial reports make based on those reports.

The Group applies the SLFRS S1 materiality principle to ensure its sustainability-related financial disclosures focus on matters that could reasonably be expected to affect the Group’s prospects and thereby influence decisions made by existing and potential primary users. In line with this, the Group’s materiality assessment focuses on the SRROs with a direct or indirect financial impact on the Group's prospects, considering both current and anticipated effects.

While SLFRS Sustainability Disclosure Standards require disclosures based on financial materiality, the Group has mapped impact materiality alongside financial materiality to provide stakeholders with a broader view of sustainability considerations as presented in the section on Material Matters

Financial materiality thresholds

The financial materiality assessment integrates both quantitative and qualitative factors to determine the significance of potential financial effects arising from the CRROs, employing a scoring system that evaluate the likelihood and impact/severity of each CRRO.

The following thresholds were applied to determine the impact/severity of the CRROs during the reporting period:

Quantitative and Qualitative criteria for determination of financial materiality

Table – 26

| Quantitative criteria | Qualitative criteria |

| Impact on Common Equity Tier I Capital (CET I): The Group uses the impact on CET1 capital to determine financial materiality, with classifications as follows:

|

|

This dual approach ensures comprehensive materiality determination by capturing both measurable financial impacts and strategic and regulatory considerations that may not yet be quantifiable but could significantly influence the decisions of the primary users of general-purpose Financial Statements.

5. Functional currency

These SLFRS Sustainability-related Financial Disclosures are presented in Sri Lankan Rupees, the Group’s functional and presentation currency.

6. Sources of guidance

Where applicable, the Group has considered guidance from following frameworks and standards, in identifying and disclosing CRROs.

- SLFRS S1 – General Requirements for Disclosure of Sustainability-related Financial Information

- SLFRS S2 – Climate-related Disclosures

- SASB Standards

- Commercial Banks Sustainability Accounting Standard (Version 2023 –12)

- Central Bank of Sri Lanka’s (CBSL) Sustainable Finance Roadmap 2.0

- Guidelines on Sustainability and Climate Related Financial Disclosure For Banks and Financial Institutions issued by the Bangladesh Bank Sustainable Finance Department

- Nationally Determined Contributions (NDCs) 3.0 (2026-2035) – Sri Lanka

- Bangladesh’s Third Nationally Determined Contribution (NDC 3.0)

- United Nations Environment Programme Finance Initiative (UNEP FI)

The Group has identified its CRROs by applying the guidance referenced above, incorporating both external evidence and the Bank-specific data.

7. Time horizon (SS – 1.2)

The impact of CRROs can be significant and far-reaching, potentially affecting the Group’s portfolio and financial performance across short, medium, and long-term horizons. Given the inherent uncertainty around the timing and scale of climate-related effects, the Group has adopted the following timeframes for risk assessment.

Time horizons

Table – 27

| Time Horizon | Period | Definition |

| Short term (S) | 1 year | Financial year 2026 |

| Medium term (M) | 2 to 5 years | Financial years 2027 to 2030 |

| Long term (L) | Beyond 5 years | Beyond financial year 2030 |

The short-term horizon aligns with the Group’s annual budgeting cycle and detailed financial planning. The medium term corresponds with the Group’s five-year financial, capital, and funding strategies. The long-term horizon is defined as greater than five years, providing the flexibility needed to assess emerging SRROs across a broader range of future scenarios.

8. Connected information

This section uses cross-references and navigation icons as shown below to highlight the connections between the CRROs and the rest of the disclosures.

Connections between different CRROs

Connections within its climate related financial disclosures

Connections across climate related financial disclosures, Annual Financial Statements, and sections in the Integrated Report.

Where disclosures are presented elsewhere in the Integrated Annual Report, the specific sections and page references are indicated.

9. Transitional reliefs

The Bank has applied the following transition reliefs permitted by SLFRS S1 and SLFRS S2 in preparing the SLFRS Sustainability-related Financial Disclosures for the year 2025.

- SLFRS S1 – Disclosure of information on only climate-related risks and opportunities:

In the first annual reporting period in which an entity applies this Standard, the entity is permitted to disclose information on only climate-related risks and opportunities (in accordance with SLFRS S2) and consequently apply the requirements in this Standard only insofar as they relate to the disclosure of information on climate-related risks and opportunities.

- SLFRS S1 – Disclosure of comparative information:

In the first annual reporting period in which the entity applies this Standard, it is not required to disclose comparative information about its climate-related risks and opportunities; and in the second annual reporting period in which the entity applies this Standard, it is not required to disclose comparative information about its sustainability-related risks and opportunities, other than its climate-related risks and opportunities.

- LFRS S2 – Disclosure of Scope 3 greenhouse gas emissions:

Entities must initially report only Scope 1 and Scope 2 emissions. Full compliance with Scope 3 emissions, becomes mandatory two years after the initial application date.

- SLFRS S2 – Disclosure of qualitative information regarding anticipated financial effects of

climate-related risks and opportunities:

Entities are permitted to defer the disclosure of qualitative information regarding anticipated financial effects for a period of two years following the mandatory application of the standard.

- SLFRS S2 – Disclosures on Climate resilience:

Relief period of two years is granted to apply the requirements from the date of mandatory application to fully comply with climate resilience disclosure requirement.

10. Significant judgements, uncertainties and proportionality

10.1 Significant judgements, and uncertainties

Sustainability-related financial disclosures presented in this section involve the application of significant professional judgement and estimation, due to the inherent uncertainty, forward-looking nature, and data limitations associated with the CRROs.

The Group operates in a dynamic financial landscape where CRROs present significant forward-looking uncertainties. In line with the requirements of SLFRS S2, the Group recognises the following contextual challenges:

- Climate-related transition risks arise from shifts in policy, technology, market conditions, and consumer preferences, creating uncertainty about the impact on business models and borrowers’ financial performance.

- Physical climate risks stem from extreme weather events and long-term environmental changes, with uncertain timing and severity that can affect operations, assets, and supply chains.

- Opportunities from green projects and low-carbon technologies are uncertain due to the pace of market adoption, evolving regulations, and technological developments.

- Business continuity has certain operational and third-party dependencies for critical infrastructure and service providers and climate events can create correlated operational and credit stresses.

- Limited availability of customer-level, asset-specific, and geographically detailed data creates uncertainty in accurately modeling climate risks.

- Rapidly evolving expectations from regulators, investors, and international institutions create uncertainty in aligning with global sustainability standards and maintaining credibility.

In light of these challenges, judgements are applied in the following areas:

Significant judgements and uncertainties

Table – 28

| Category | Assessment Methodology | Key Limitations & Uncertainties | |

| a. | Materiality | The assessment evaluates whether specific CRROs could have a material impact on the Group’s cash flows, access to finance, or cost of capital. A scoring system was applied, combining likelihood with both quantitative and qualitative impact criteria to determine their financial materiality. Refer Table 26 Quantitative and Qualitative criteria for determination of financial materiality on SLFRS Sustainability-related Financial Disclosures. |

|

| b. | Time horizon classification |

Time horizons are defined to align with the Group’s strategic planning cycle. Refer Table 27 Time Horizons on SLFRS Sustainability-related Financial Disclosures. |

|

| c. | Assessment of assets vulnerable to climate-related physical risk (floods) |

|

|

| d. | Assessment of assets vulnerable to climate-related transition risk |

and Table 37: Key Findings – Vulnerability to climate-related transition risk. |

While the assessment provides a useful high-level overview, it has inherent limitations,

including: – Reliance on broad sector classifications, that may overlook granular company-specific activities. – Use of global data that may not reflect local conditions. – Sector sensitivity scoring may not precisely capture emission intensity of borrowers and specific future conditions such as changes in policy, technological and customer preferences. – Not capturing the transition preparedness or strategies of individual borrowers. The Bank is in the process of computing its financed emissions. This initiative will provide a more granular, data-driven foundation to better estimate the portion of assets vulnerable to climate-related transition risk, moving beyond reliance on Sector sensitivity scoring. |

| e. | Significant risk of material adjustments to carrying value of assets and liabilities within the next annual reporting period (i.e. in 2026) | For physical climate risks, the Bank evaluated the sensitivity of its loans and advances

portfolio to flood risk using heatmaps, as outlined in section (c) above. Key customer exposures were further overlaid onto floodplain hazard maps, providing a detailed, location-specific view of high-risk areas. Transition risks were evaluated based on evolving policies, regulations, and market developments supporting the low-carbon transition, including the trajectory of announced government policies and phased regulatory measures. Refer Figures 55 to 58 |

|

10.2 Proportionality

SLFRS Sustainability Disclosure Standards include proportionality mechanisms to address concerns that it may be challenging for the Group to apply specific requirements within the Standards.

These proportionality mechanisms include:

- The consideration of the Bank’s skills, capabilities and resources

- The use of all reasonable and supportable information that is available to the Bank at the reporting date without undue cost or effort

Instances where the above application is used in this section are;

- Identification of CRROs

- Determination of the scope of value chain

- Assessment of percentage of assets vulnerable to climate-related risks as described in Notes 10.1(c) and 10.1 (d) in the Table 28

- Assessment of Significant risk of material adjustments to carrying value of assets and liabilities within the next annual reporting period, as described in Note 10.1 (e) in the Table 28.

11. Statement of compliance

The Group’s sustainability disclosures have been prepared in compliance with the SLFRS Sustainability Disclosure Standards issued by the Institute of Chartered Accountants of Sri Lanka, applying the Transitional Reliefs as outlined in Note 9 – Transitional Reliefs. Accordingly, this report presents a comprehensive set of sustainability-related financial disclosures for Commercial Bank of Ceylon PLC and its subsidiaries (collectively, ‘the Group’) for the year ended December 31, 2025.

Governance

1. Board oversight (SG – 1.1)

1.1 Ultimate accountability

The Board of Directors of the Bank assumes ultimate responsibility for oversight of SRROs and for ensuring their integration into strategy, risk appetite, capital allocation, and performance management.

1.2 Delegation to committees

To ensure effective governance of SRROs, the Board delegates oversight responsibilities to its committees, with clearly defined accountabilities to strengthen governance. The framework reflects regulatory primacy, with the Board Integrated Risk Management Committee (BIRMC) overseeing sustainability-related risks that affect the Bank’s safety and soundness, while the Board Sustainability Committee (BSC) provides strategic direction and advisory stewardship on Sustainability and ESG matters, with a clear “risk sign-off” dependency, where relevant.

These committees operate under a coordinated structure with cross-membership and consultation mechanisms to ensure clarity of roles, single-point accountability, and efficient escalation of material matters to the Board.

The roles of the key committees are as follows:

- Board Integrated Risk Management Committee (BIRMC) – apex oversight

of SRROs

The BIRMC retains primary responsibility for integrating SRROs into the Bank’s enterprise risk management framework, including risk appetite, policies, limits, stress testing, and scenario analysis used for risk governance and capital planning.

The Committee:

- Evaluates SRROs identified by Management and informed by the BSC.

- Provides independent challenge on risk identification, assessment, prioritisation, and monitoring.

- Ensures SRROs are embedded alongside operational and financial risks.

- Facilitates the timely escalation of material SRROs to the Board, keeping it informed of key risk exposures, trade-offs, and emerging regulatory developments.

- Reviews risk-related sustainability disclosures to ensure consistency with the enterprise risk management framework.

Detailed information on the Charter of the BIRMC is provided in the Report of the Board Integrated Risk Management Committee.

- Board Sustainability Committee (BSC) – Advisory stewardship on

Sustainability and ESG matters

The BSC assists the Board by providing strategic direction and advisory guidance on Sustainability and ESG matters, in alignment with its mandate. The Committee operates in a non-executive, advisory capacity and does not exercise executive or risk management authority unless specifically delegated by the Board.

The BSC reviews management proposals relating to the integration of sustainability and ESG considerations into the Bank’s strategy, governance and operations, and makes recommendations to the Board, as appropriate.

The Committee:

- Provides strategic guidance on the Bank’s sustainability strategy, roadmap, targets, KPIs and overall governance maturity.

- Reviews sustainability-related policies, frameworks and management proposals, and recommends improvements or alternative approaches to the Board.

- Provides guidance on sustainability-related disclosures, including compliance with SLFRS Sustainability Disclosure Standards with emphasis on transparency, credibility, materiality governance and assurance readiness.

- Reviews and provides recommendations on the Bank’s Climate Transition Plan, sustainable finance initiatives and net zero ambitions.

- Encourages adoption of ESG best practices across stakeholders including clients, vendors and suppliers, in alignment with national priorities and regulatory expectations.

Maintains appropriate liaison with the BIRMC on material SRROs that may affect the Bank’s risk profile.

Detailed information on the Charter of the BSC is provided in the Report of the Board Sustainability Committee .

- Board Audit Committee (BAC) – disclosure integrity and

assurance.

The BAC oversees the internal control environment for sustainability data and disclosures, internal audit reviews of non-financial reporting controls, and the scope and results of independent external assurance over SLFRS Sustainability Disclosure Standards.

- Board Human Resources & Remuneration Committee (BHRRC) –

accountability through incentives.

The BHRRC, in collaboration with the BSC reviews and recommends sustainability-linked KPIs for Executive Directors, corporate management, and senior leadership, and ensures appropriate linkage between SRRO outcomes and remuneration.

- Board Nominations & Governance Committee (BNGC) – Board

competency and succession.

The BNGC, in liaison with the BSC, oversees Board composition, ensuring appropriate skills and experience in sustainability, climate change, and stakeholder governance, and arranges training and capacity development for the Board of Directors where needed.

1.3 Escalation and reporting (SG – 1.3)

During the year, the management commenced the implementation of a framework to escalate material SRROs, such as breaches of climate or ESG-related thresholds/issues, significant regulatory changes, or reputational issues to the BIRMC. As this process matures, the management intends to report these issues to the full Board on a quarterly basis, based on recommendations from the BIRMC. The initial outcomes and insights from the BIRMC discussions were presented to the full Board to begin providing an integrated view of emerging risks, opportunities, and strategic trade-offs.

Following the formation of the BSC, the Bank has implemented an enhanced escalation framework. Under this framework, the BSC reviews strategic sustainability matters and significant ESG developments from a strategic and governance perspective and provides advisory inputs and recommendations to the Board. Where such matters have implications for the Bank’s risk appetite, prudential limits, capital planning or overall risk profile, they are referred to the BIRMC for consideration within the Bank’s enterprise risk management framework. The BSC maintains appropriate liaison with the Chair of the BIRMC to ensure timely referral and coordination on material SRROs. Extraordinary sustainability events with potential material financial or reputational impact are escalated promptly to the Chair of the BIRMC and the Board Chair, independent of the regular meeting cycle, to ensure timely oversight and response.

Insights from the BSC’s deliberations, together with BIRMC discussions where relevant, are reported to the full Board to provide an integrated view of emerging SRROs and strategic trade-offs. As the process matures, structured quarterly reporting to the Board will continue to strengthen governance, transparency and accountability. This framework ensures that SRROs are effectively managed in alignment with the Bank’s risk appetite, governance standards, and regulatory requirements, while leveraging the specialised sustainability expertise of the BSC.

1.4 Skills and competencies (SG – 1.2)

The members of the BIRMC and BSC bring a diverse and complementary set of skills in banking, financial services, capital markets, corporate finance, risk management, audit, compliance, and ESG integration. Their broad exposure across multiple sectors and geographies enhances the Bank’s ability to oversee SRROs and implementation of the Bank’s sustainability strategy. (Refer to the Board of Directors and Profiles for more information)

The Board and its Committees maintain access to internal and external expertise to support their SRRO oversight, including periodic deep-dives and training on evolving standards and market practices. During the year, the Bank conducted a skills and competencies gap self-assessment focused on SRRO oversight. The outcomes will inform targeted capacity-building initiatives and further strengthen the Board and its committees’ contribution to advancing the Bank’s sustainability objectives.

1.5 Overseeing and monitoring of SRROs (SG – 1.4, SG – 1.5, SG – 1.6)

During the year, the Board, primarily through the BIRMC, exercised oversight of SRROs, ensuring their systematic identification, assessment, and management across the Bank’s strategic and operational frameworks. This oversight was carried out through periodic reviews of key policies and frameworks, including the Climate Risk Management Policy and Procedure, Environmental and Social Risk Management Policy, ESG Policy, Green Financing Policy, Financed Emissions Framework, and progress on the Bank’s Climate Transition Plan. To support informed decision-making, the BIRMC was provided with comprehensive quarterly reports from the management, enabling it to monitor emerging trends, evaluate the effectiveness of mitigation measures, and track the Bank’s progress toward its broader sustainability and climate-related objectives while adapting to evolving regulatory expectations.

In overseeing the Bank’s strategy, the Board and its Committees, take SRROs into account by embedding ESG integration and Responsible Banking as a key strategic enabler. The BSC reviews SRROs, ensuring they inform strategic priorities, major transactions, and capital allocation, while supporting the Board in balancing financial, environmental, and social outcomes.

In this enhanced governance structure, the BIRMC will focus on overseeing SRROs from a risk management perspective, monitoring those that affect the Bank’s risk appetite, prudential limits, and overall risk profile. It will coordinate with the BSC to ensure material sustainability risks are identified, assessed, and managed within the Bank’s risk framework, providing assurance to the Board on effective risk mitigation and alignment with regulatory requirements and strategic objectives.

In addition, the BHRRC, in consultation with the BSC and the BIRMC, is progressively phasing in the integration of prioritised KPIs connected to SRROs into the performance and variable remuneration frameworks across all organisational levels from Executive Directors, Corporate and senior management, to all staff thereby strengthening accountability and ensuring strategic alignment with the Bank’s sustainability objectives and risk management frameworks.

Board Activities in 2025: Decisions and policy endorsements for strategic

sustainability integration

Table – 29

| Topic | Responsible Committee(s) | Board activity | Key decisions/Outcomes |

| BIRMC Charter | Board, BIRMC | Reviewed amendments to include SRRO oversight explicitly. | Approved updated Charter, Formalised SRRO oversight. |

| Climate Risk Management Policy and the Climate Risk Management Procedure | Board, BIRMC | Evaluated the newly developed Climate-Risk Management Policy and Procedure, including climate-risk identification, scenario analysis, risk limits, mitigation strategies, and alignment with international best practices. | Approved the implementation of Climate Risk Management Policy. Approved the implementation of Climate Risk Management Procedure. |

| ESG Policy – Bank | Board, BIRMC | Reviewed enhancements on governance, stewardship, and stakeholder engagement. | Approved the revised ESG Policy, mandating its integration into operational and strategic frameworks. |

| Financed Emissions Framework – Bank | Board, BIRMC | Reviewed the Framework to measure and manage GHG emissions associated with loans and investments. | Approved the adoption of the Framework and aligned the methodology to recognise market practices and staged portfolio coverage targets. |

| Green Bond Issuance | Board | Evaluated and approved the Rs. 15 Bn. green bonds issuance during the year, including use of proceeds, governance and investor demand. | Approved the Sustainable Bond Framework. Approved the issuance of Green Bond |

| Materiality (SLFRS S1/S2) |

Board, BIRMC | Reviewed 2025 methodology and prioritised SRROs. | Approved the methodology and outcome of the assessment in compliance with SLFRS S1/S2. |

| SLFRS Sustainability-related Financial Disclosures-2025 | Board, BIRMC, BAC, BSC | Analysed the proposed disclosures for completeness and alignment with SLFRS S1/S2. | Approved disclosures for inclusion in Annual Report 2025. |

| Formation of a Board Sustainability Committee | Board | Ratified the Charter of the newly formed BSC, defining its authority, roles, responsibilities, and operating procedures for oversight of SRROs and ESG matters. | Approved the BSC Charter. |

2. Management’s role (SG – 2.1)

2.1 Executive Sustainability Committee (ESC)

The ESC, comprising senior management from risk, business lines, finance, strategy, is responsible for executing the Board-approved sustainability strategy. It integrates SRROs into the Bank’s corporate strategy, business model and value chain (origination, underwriting, portfolio management, and operations). The ESC:

- Guides the identification, assessment, and management of SRROs, ensuring they are integrated into the Bank’s corporate strategy, decision-making, and value chain.

- Ensures sustainability practices and disclosures comply with SLFRS S1/S2 standards, backed by robust internal controls and independent assurance to maintain transparency, accuracy, and stakeholder trust.

- Ensures the ESC and relevant teams have the necessary skills, expertise, and resources to effectively oversee and implement sustainability strategies and respond to emerging SRROs.

- Evaluates and recommend necessary modifications to systems, processes, and policies to facilitate effective sustainability implementation across the Bank.

- Reports quarterly to the BIRMC and provides interim briefings for any material events.

Following the formation of the BSC, material SRROs, strategic sustainability matters, and urgent ESG events will be submitted to the BSC, which reviews and provides recommendations to the Board while coordinating with BIRMC on associated risks.

The ESC is composed of the following members:

2.2 Sustainability Working Committee (SWC)

Reporting to the ESC, SWC is responsible for executing the Bank’s sustainability agenda, encompassing the following key mandates:

- Ensuring the Bank’s sustainability practices and reporting comply with the SLFRS Sustainability Disclosure Standards.

- Identifying sustainability-related material topics pertinent to the Bank’s business model and value chain through a comprehensive materiality assessment process to improve stakeholder communication.

- Development and implementation of the Climate Transition Plan, ensuring alignment with organisational goals and timelines.

2.3 Management controls and their integration across internal functions (SG – 2.2)

The management oversees the SRROs through a comprehensive framework of Board-approved policies and

procedures, including the ESG Policy, Climate Risk Management Policy and Procedure, and Environmental

and Social Risk Management Policy. Controls over SRROs are embedded across operational, credit, and risk

management functions, ensuring consistency with the Bank’s policies, risk appetite, and strategic

objectives. These processes are continuously enhanced to support the full implementation of the SLFRS

Sustainability Disclosure Standards by 2027, as stated in the Directors’

Statement on Internal Control

over Financial Reporting and Risk Management .

3. Culture & employee engagement:

Fostering a robust culture of employee engagement is critical to building resilience against

climate-related risks and capitalising on emerging opportunities. The Bank promotes this culture through

initiatives such as the Future Force Group, a cross-functional and multi-level employee forum that

serves as a dynamic incubator for innovative ideas. By integrating frontline insights and diverse

perspectives into decision-making, the Bank reinforces sustainability values in everyday behaviors,

strengthens accountability for ESG outcomes, encourages cross-functional collaboration, and supports

continuous learning and innovation to respond effectively to evolving climate and sustainability

challenges.

4. Reporting standards and frequency (SG – 1.3)

- Standards – Public reporting is prepared in accordance with SLFRS Sustainability Disclosure Standards (SLFRS S1 and SLFRS S2), Sustainability Accounting Standards Board (SASB) Standards and in line with the principles of the International <IR> Framework of the IFRS Foundation.

- Frequency – The Bank on a quarterly basis reports on the status of SRROs to the Board via the BIRMC. The Bank publishes comprehensive disclosures on CRROs in the Annual Report, with material changes reported in the Interim Financial Statements, if any. Additional market updates and disclosures are provided as required (e.g., green bond impact reporting).

5. Continuous improvement

The Bank will continue to strengthen governance over SRROs through:

- Periodic skills assessments and training for Directors and Executives;

- Enhancement of data architecture and controls;

- Progressive expansion of external assurance coverage; and

- Transparent stakeholder engagement to inform strategy and disclosures.

Risk management

1. Climate-related risks management overview

The Bank for International Settlements (BIS) and the Network for Greening the Financial System (NGFS) which is a network of central banks and supervisors, have emphasised that climate-related risks present a source of systemic financial risk. These risks are broadly categorised into Physical and Transition risks, each with distinct yet interconnected transmission channels into the Bank's financial health and operational stability.

As illustrated in Figure 52, physical risks arise from acute events as well as chronic shifts in climate patterns, which can disrupt economic activity and increase credit and operational losses. Transition risks, on the other hand, stem from the shift toward a low-carbon economy, including changes in regulation, technology, market preferences, and reputational expectations.

Climate-related risks Figure – 52

Climate Risks

Transition risks

Risks related to the process of transitioning away from reliance on fossil fuels and towards a low-carbon economy

Physical risks

Risks which arise from the physical effects of climate change and

environmental degradation

Acute

Event-driven, increase of frequency or severity due to climate change

Chronic

Long-term shifts in climate patterns

1.1 Climate-related opportunities

In parallel with identifying risks, the Bank proactively seeks to identify and capture climate-related opportunities that can support the transition to a sustainable economy while strengthening its long-term resilience. Such opportunities include financing renewable energy, energy efficiency, and green infrastructure projects, as well as developing innovative sustainable finance products to meet the evolving needs of clients.

The Bank acknowledges that, unless these opportunities are properly understood, assessed, and integrated into its strategy, they could evolve into risks such as loss of market share, reputational setbacks, or missed investment potential.

1.2 Phased approach to integration of climate risk management across the group

During 2025, the Bank established a comprehensive Climate Risk Management Policy, applicable to the Bank and its subsidiaries. In parallel, a comprehensive Climate Risk Management Procedure was developed for the Bank to provide the strategic foundation for integrating climate risk into its operational and broader Risk Management frameworks.

The Climate Risk Management Procedure is a structured approach to climate risk management, encompassing risk identification, impact assessment, implementation of mitigation measures, and continuous monitoring. This systematic methodology is applied consistently at both the individual customer and portfolio levels, as shown in the Figure 53 and Figure 54 for Climate related physical risks and Climate-related transition risks. For physical risks, the process prioritises hazards such as floods, droughts, storms, and landslides, based on their historical frequency and the extent of disaster-related losses in the Bank’s operating geographies. In addressing transition risks, the analysis focuses on four key drivers; policy and legal, technology, market and reputation risks.

Climate-related physical risk management: Customer and portfolio-level

approach

Figure – 53

(SRM – 1)

Customer level

Identify the customer assets, geographical locations and financial

values

Physical predisposition of customer to adverse effects of physical

climate

hazards

Engage with customer to prevent, respond or recover from physical

climate

hazards

Track the customer’s adaptation efforts and evaluate how effective

they are

over time

Identify the Physical Climate Hazards

↓

Identify the Exposure

↓

Assess the Sensitivity

↓

Assess the Adaptation

↓

Monitor

Identify geographical distribution of all assets in the portfolio

Identify the sectors or types of assets most financially sensitive to

physical climate hazards

Apply risk reduction strategies at the portfolio level

Regulatory review and update portfolio exposure to physical risk

Portfolio level

Climate-related transition risk management: Customer and

portfolio-level approach Figure – 54

(SRM – 1)

Customer level

Evaluate the customer’s exposure to policy changes, market shifts,

and technological developments

Quantify how transition risks may impact the customer’s finances

Assist the customer to seize growth opportunities in the low-carbon

economy

Engage with customers to set emissions targets and invest in green

technologies or practices

Track the progress of implementation of the customer’s transition

plan

Regularly review the customer’s progress in alignment with

national/international climate targets

Transition Risk Drivers

↓

Evaluate

↓

Opportunities

↓

Mitigation

↓

Implementation

↓

Monitor

Assess the carbon intensity and exposures of the portfolio to

requirements of the Climate Policy

Analyse the broader transition risks exposure

of the portfolio

Model financial benefits of supporting

transition-aligned sectors

Identify and prioritise sectors or assets for

green investments

Incorporate transition plan into overall strategy

Monitor the portfolio’s alignment with national/international climate

targets

Portfolio level

2. Identification of climate-related

risks (SRM – 1)

Climate-related risks are identified along the following parameters;

- Portfolio composition, including detailed screening by sector, geography, and loan type.

- Geospatial vulnerability, utilising mapping of collateral and borrower locations against specific climate hazard maps for floods, cyclones, landslides, and droughts.

- Sector-based transition dynamics, evaluating carbon intensity, policy exposure, and potential technology or market disruptions.

- Temporal shifts in expectations, conducted through continuous stakeholder and regulatory horizon assessments over short, medium, and long-term horizons.

In identifying and disclosing CRROs, the Bank has also considered relevant Sources of Guidance, as set out in Note 6 – Sources of Guidance.

Identification of climate risk is incorporated across the entire credit lifecycle and the credit risk management process and this process is integrated into both portfolio-level analysis and individual client engagement, in line with the Bank’s Climate Risk Management Policy and Procedures.

The Bank has developed a roadmap to conduct climate-related scenario analysis and is in the process of building internal capacity to support this strategic initiative. During this developmental phase, the Bank has elected to apply the two-year relief period provided under the transitional reliefs outlined in Note 9 – Transitional Reliefs.

3. Assessment of climate-related risks (SRM – 1)

3.1 Climate-related physical risk assessment

The Bank evaluates the potential impact of major physical climate hazards on its portfolio by analysing their effects on borrowers’ businesses, collaterals, sectoral concentrations, and geographic exposures, in line with the Bank’s Climate Risk Management Procedures. The Bank prioritises hazards such as floods, droughts, storms, and landslides, based on their historical frequency and impact to the country’s annual disaster-related losses.

At the portfolio level, physical climate risks are evaluated through geospatial heat mapping, integrating external climate hazard data (e.g., from the World Bank and ThinkHazard!) with sector sensitivity scores based on IFC proprietary metrics. The likelihood of a climate hazard is derived from historical frequency and probability of occurrence, while the severity is evaluated in a broad-based manner, reflecting the potential consequences for borrowers’ operations. This broad-based assessment is embedded within the IFC sector sensitivity scoring, which incorporates sector-specific characteristics and vulnerabilities.

During the year, the Bank developed an internal tool that overlays the geographical locations of customers covering over 40% of the loan portfolio as of December 31, 2025. This tool will progressively serve as a primary reference point for assessing climate risk on an ongoing basis, guiding customer exposure levels, and ensuring that physical climate risk considerations remain embedded within the Bank’s portfolio-level risk management framework.

Following Cyclone Ditwah, a real-world physical climate stress scenario, a comprehensive review of the physical climate risk framework was initiated. By comparing hazard intensity assumptions with observed flood, landslides, and wind impacts, the physical climate risk assessment methodology is being refined. This enhanced assessment establishes a foundation for climate stress testing and enables the Bank to evaluate and strengthen its risk response measures, ensuring that its climate strategy remains proactive, adaptive, and operationally resilient.

Building on the Bank’s portfolio-level screening, borrower-level assessments are conducted to evaluate the vulnerability of individual customers to physical climate hazards. This granular analysis complements the broader portfolio assessment, enabling the Bank to identify material risks embedded in specific credit exposures that may not be fully captured at the macro level.

To translate portfolio-level insights into actionable borrower-level analysis, the Bank conducts enhanced due diligence at the individual borrower or facility level. This is particularly applied to exposures exceeding a predetermined threshold and have a remaining contractual tenor above one year, as well as to higher-risk sectors, in line with the Bank’s Climate Risk Management Procedure and sector-specific guidance. The threshold determination and any exceptions are subject to independent review by the Integrated Risk Management Department and oversight through established credit governance frameworks. This targeted approach allows the Bank to refine risk scores by incorporating borrower-specific characteristics, including any adaptive measures the borrower may have implemented to manage climate-related impacts.

3.2 Climate-related transition risk assessment

At the portfolio level, climate-related transition risks are assessed using UNEP FI sector sensitivity scores to identify sectoral gross exposure to policy, market, and technological transition risks, as specified in the Bank’s Climate Risk Management Procedures. This assessment focuses on potential impacts arising from the transition to a low-carbon economy, including direct and indirect emissions-related costs, low-carbon capital expenditure requirements, and potential revenue impacts across lending sectors. Each sector is assigned a corresponding transition sensitivity score, enabling the Bank to identify transition risk concentrations and assess the overall transition risk profile of the portfolio.

Complementing the portfolio-level assessment, the Bank conducts borrower-level climate-related transition risk assessments for exposures exceeding a predetermined threshold, based on loan size, tenure, or overall exposure in the portfolio.

These assessments focus on the borrower’s emissions profile, reliance on carbon-intensive activities, and readiness to adapt to evolving policy, market, and technological changes. Transition risk is evaluated using UNEP FI data and internationally accepted taxonomies, supplemented by borrower-specific information, where available.

Key assessment factors include direct and indirect emissions (assessed using borrower-level data or sector benchmarks as proxies), carbon cost exposure from potential future carbon pricing mechanisms, low-carbon readiness reflected through green capital investments and transition strategies, and stranded asset risk arising from reliance on assets vulnerable under low-carbon transition scenarios.

Where borrowers demonstrate ability to mitigate transition impacts, the corresponding transition risk score may be adjusted to reflect mitigated outcomes, ensuring that borrower-level assessments capture both inherent transition risks and the effectiveness of mitigation measures, thereby supporting informed credit decisions and ongoing risk monitoring.

4. Prioritisation of climate risk relative to other types of risks (SRM – 1)

The Bank prioritises climate risk by integrating it into its overall risk management framework, recognising its increasing significance for financial stability and operational resilience. This prioritisation is guided by global assessments, such as the World Economic Forum's Global Risks Report 2025, which identifies environmental risks, including extreme weather events and biodiversity loss as among the most severe threats over the next decade.

To ensure a systematic and consistent approach, the Bank applies a structured prioritisation framework that evaluates all risks, including climate risk, across multiple dimensions as shown below.

- Integration into Risk Management Framework: Climate and broader environmental and social (E&S) risks are fully incorporated into the Bank’s Internal Capital Adequacy Assessment Process (ICAAP) and wider risk management through qualitative scorecard-based assessments.

- Potential financial impact: Assessing the extent to which climate-related events could affect the Bank’s financial position and overall financial performance.

- Operational criticality: Evaluating how climate events may disrupt critical operations, processes, or services.

- Strategic alignment: Considering how the climate risk aligns with or affects the Bank’s strategic objectives and long-term sustainability goals.

- Velocity of manifestation: Analysing how quickly the risk could materialise and affect the Bank.

- Consistency with risk appetite: Ensuring the risk remains within the boundaries of the Bank’s defined risk appetite and tolerance levels.

Through this structured evaluation, climate risk is embedded within traditional risk categories and prioritised alongside other key risks, enabling the Bank to proactively manage exposures and drive sustainable growth amid an evolving environmental and regulatory landscape.

This strategic integration is critical not only for ensuring regulatory compliance but also for mitigating the growing reputational risk associated with an inadequate climate response, which the Bank has identified as a material climate risk. (Refer Figure 57: Reputational Risk from Inadequate Climate Response).

5. Monitoring of climate risks

The Bank’s process of monitoring of climate risk is governed by its Climate Risk Management Policy and the Procedure. The Bank is in the process of enhancing its data infrastructure in phases to improve reporting capabilities, enabling detailed tracking of material CRROs. Monitoring of physical risks will be progressively refined with expanded portfolio coverage through system developments. Further, transition risk metrics such as carbon intensity, Weighted Average Carbon Intensity (WACI) will be developed following the completion of financed emissions computation. These metrics will be monitored as part of the Bank’s key risk indicators in the time to come.

6. Changes in climate risk management processes compared with the previous reporting period (SRM – 1.2)

During 2025, the Bank took steps to lay a structured foundation for climate risk management. This included developing a dedicated Climate Risk Management Policy and a Procedure, integrating climate risk alongside E&S considerations into the ICAAP and broader risk framework through qualitative scorecard-based assessments, and introducing data-driven metrics and disclosure practices.

7. Process for identifying, assessing, and monitoring climate-related opportunities (SRM – 2)

The Bank employs a systematic process to identify, assess, prioritise, and monitor climate-related opportunities as guided by its Climate Risk Management Policy and the Procedure, and the Green Finance Policy. The Bank proactively identifies climate-related opportunities by monitoring national policy incentives such as Sri Lanka’s NDCs and the CBSL Green Finance Taxonomy, evolving market demand for sustainable products, and technological innovations that enable renewable energy, energy efficiency, and climate-resilient infrastructure. Performance is measured using metrics such as the portfolio growth, and the alignment of lending with recognised taxonomies. Further, the ongoing borrower engagement, including regular assessment of client transition or adaptation plans forms a critical part of monitoring, strengthening both client resilience and the de-risking of the Bank’s portfolio. Through the materiality assessment process for SLFRS Sustainability-related Financial Disclosures, the Bank identified the Sustainable Finance as a material climate-related opportunity. (Refer Figure 58: Sustainable Finance Opportunity).

The Bank recognises climate-related scenario analysis as a critical tool for identifying CRROs. To ensure preparedness for this requirement which becomes mandatory effective from January 01, 2027, the Bank has developed a roadmap to ensure timely compliance while building internal capabilities.

8. Integration of climate risk with overall risk management process (SRM – 3)

The Bank integrates CRROs into its overall risk management process through a structured risk governance framework based on the Three Lines of Defense. (Figure 68, Risk Governance and Management Section.

First Line of Defense – Business and Operational Units: Business units, relationship managers, and credit officers own and manage climate risks in day-to-day operations. They identify and assess risks at customer engagement and transaction origination, conduct initial due diligence for facilities above a pre-defined internal threshold, implement mitigation actions including covenants, guidance on adaptation measures, and pursue Green Financing opportunities while maintaining internal controls aligned with the Bank’s Climate Risk Management Policy.

Second Line of Defense – Integrated Risk Management Department: Led by the Chief Risk Officer, provides independent oversight, guidance, and challenge. It develops the Climate Risk Management Policy, associated procedures, validates First Line risk assessments, monitors portfolio-level exposures, provides tools and methodologies for consistent risk evaluation, and reports material findings to the BIRMC.

Third Line of Defence – Internal Audit Function: The Internal Audit Department provides independent assurance to the BAC on the effectiveness of governance, risk management, and controls over climate risks. It audits the design and operation of controls, validates that risks are adequately identified and managed, evaluates assessment methodologies and data quality, and reports findings with recommendations for improvement.

This Three Lines of Defense structure ensures that CRROs are systematically identified, assessed, monitored, and integrated into the Bank’s overall risk management framework.

Strategy

1. Our context

The Group recognises that climate change is one of the most significant and far-reaching challenges facing the financial services sector. As a leading financial institution in Sri Lanka, the Bank is directly exposed to both physical and transition risks arising from climate change, while also being uniquely positioned to drive the country’s transition to a low-carbon and climate-resilient economy.

The Bank’s climate strategy is designed to address both the physical and transition risks of climate change through adaptation and mitigation measures as detailed below.

Adaptation

(Managing Physical Climate Risks)

Safeguarding financial resilience

Strengthening the Bank’s ability to withstand climate-related physical risks, such as floods, storms, and other extreme weather events, to protect its assets, operations, and risk profile.

Supporting client climate adaptation

Assisting clients in building resilience to climate impacts through advisory services, risk assessments, and climate-resilient financing solutions.

Mitigation

(Enabling the Low-Carbon Transition)

Supporting client transition

Helping clients reduce carbon intensity, align with decarbonisation pathways, and adopt low-carbon technologies and practices.

Seizing opportunities in sustainable finance

Expanding financing for renewable energy, green and blue projects, and other sustainable initiatives that contribute to emissions reduction and a low-carbon economy.

To advance this strategy, emphasis is placed on strengthening credit underwriting standards, embedding climate scenario analysis into portfolio management, and progressively aligning exposures with Sri Lanka’s national climate commitments and internationally recognised pathways for a low-carbon transition.

By integrating sustainability into the Bank’s core lending strategy, the Bank is expanding its footprint in renewable energy, green infrastructure and climate-smart agriculture. This is supported by the Bank’s commitment to issue green bonds, adopt global disclosure frameworks, and developing a Climate Transition Plan in partnership with Development Financial Institutions (DFIs) such as the IFC.

The Bank recognises that climate strategy cannot be pursued in isolation. Accordingly, it emphasises collaboration with regulators, international lenders, industry associations, and community stakeholders to ensure an orderly and inclusive transition while supporting climate adaptation and resilience. Capacity building, investment in climate analytics and ESG data systems, transparent stakeholder communication and strategic collaboration with industry partners and stakeholders are key enablers of the Bank’s climate strategy.

1.1 Climate position statement of Commercial Bank of Ceylon PLC –

Refer Figure 39.

1.2 Climate transition plan (SS – 3.2)

The Bank is in the process of developing a comprehensive Climate Transition Plan in partnership with the IFC, aligned with national decarbonisation pathways. As the first Sri Lankan bank to join the Partnership for Carbon Accounting Financials (PCAF), the Bank commenced measuring its financed emissions (Category 15: Investments) and developed a Financed Emissions Framework during the year to guide the management and reduction of emissions associated with its lending and investment portfolios as indicated in Figure 59 – Roadmap of computation of Financed Emissions .

Core focus areas of the climate transition plan are; (SS – 3.2)

-

Establishing the foundations for transition planning

The Bank laid the groundwork for its Climate Transition Plan by establishing a baseline for financed emissions and analysing the loan portfolio to identify high carbon-emitting sectors. Portfolio alignment with national climate goals was also assessed to ensure consistency with the country’s decarbonisation pathways.

-

Accelerating Green and Blue finance

During the year, the Bank advanced its sustainable finance agenda, setting a target to achieve a Rs. 100 Bn. green financing portfolio by 2030, developing new green finance products and identifying credit exposures in carbon-intensive sectors and promoting a gradual shift toward more sustainable lending practices. (Refer Figure 19 – Green Finance). This target will be revised as the portfolio expands in the near future.

-

Strengthening capacity for climate risk management

The Bank enhanced its climate risk management capabilities by integrating climate considerations into risk governance and management procedures, identifying material exposures to carbon-intensive assets. Targeted capacity-building initiatives further strengthened the Bank’s ability to manage climate-related financial risks effectively.

2. Climate-related risks and opportunities (CRROs) (SS – 1.1, SS – 1.2, SS – 2.1, SS – 3.1, SS – 3.3, SS – 3.4, SS – 4.1)

During the year, the Bank evaluated its value chain and identified three material climate-related risks and one material climate-related opportunity that could reasonably be expected to affect the Bank’s prospects. These are set out in the Figures 55 to 58 below together with impacts and strategies.

Impact of extreme weather on borrowers’ financial capacity

Figure – 55

| Climate-related risk 01 | Extreme weather events Extreme weather events, including floods, landslides, cyclones and droughts, are becoming more frequent and severe, often exacerbated by climate change. These events pose a material credit risk to the Bank, as they can weaken borrowers’ financial capacity and increase the likelihood of loan defaults and non-performing loans. |

| Description | Climate change elevates credit risk through increased borrower default probabilities, driven by

more frequent/severe extreme weather events. Borrowers in areas prone to extreme weather face:

|

| Physical risk/Transition risk | Physical risk |

| Time period | S, M, L (Note 07 – Table 27). |

| Current and anticipated effects of those CRROs on the Bank’s business model and value chain | Current Impact The impact of Cyclone Ditwah on the Bank’s business model listed below should be considered alongside its effects on the economy, as detailed in the section Operating Environment & Outlook on Operating environment and outlook.

|

Anticipated Impact

|

|

| Where it is impacted Credit Risk Extreme weather events elevate credit risk by increasing the Probability of Default (PD), through income loss from operational disruptions, and/or the Loss Given Default (LGD), due to direct collateral damage and property devaluation. While Cyclone Ditwah served as a stress event, impacting all 25 districts in Sri Lanka, the direct physical damage was most heavily concentrated in loans utilised in Colombo, Gampaha, and Kandy Districts. As of December 31, 2025, the Bank assessed the sensitivity of its loan portfolio to climate-related physical risks, particularly floods, by combining district-level hazard classifications from “ThinkHazard!” with sector-specific sensitivity scores. This approach allowed the Bank to identify exposures in high-risk districts and vulnerable sectors, providing a robust basis for targeted risk monitoring, enhanced due diligence, and informed portfolio management decisions. Refer Table 34: Sensitivity to climate-related flood risk and Table 35: Key findings – Sensitivity to climate-related flood risk.

|

|

| Reputational Risk Extreme weather events are likely to intensify stakeholder scrutiny of the Bank’s contribution to adaptive measures and support for affected customers. However, by undertaking proactive actions such as transparent communication, flexible customer support, CSR initiatives, and active stakeholder engagement, the Bank can reinforce its reputation and strengthen resilience across the value chain. |

|

| How the Bank has responded or plans to respond to CRROs in its business strategy and decision making | Credit Risk Direct Adaptation Actions:

|

Indirect Adaptation Actions:

|

|

| How the Bank is resourcing, and plans to resource the activities | Human Capital Development: Implementing employee training on climate risk,

disaster recovery, and customer engagement. Technology Integration: Investing in data analytics, scenario modeling, and digital platforms to enhance climate risk assessments and customer communication during extreme weather events. Strategic Partnerships: Collaborating with NGOs, government agencies, industry groups, and academic institutions to support community resilience, access expertise, and develop climate risk adaptation solutions. Stakeholder Engagement: Establishing customer feedback channels and maintaining transparent communication channels with investors to align climate strategies with their expectations. Continuous Monitoring and Evaluation: Defining KPIs and conduct regular reviews to assess the effectiveness of climate risk initiatives to optimise resource allocation. |

| Progress of the plans and initiatives | Human Capital Development Training Programs: Over 500 employees participated in specialised training sessions in 2025 focused on climate risk management. Strategic Partnerships: Partnering with IFC helps leverage their expertise and resources in sustainable finance and climate risk management. Stakeholder Engagement: Organising an annual Sustainability Summit creating a platform for sharing knowledge, innovations, and strategies related to climate risk and sustainable development. |

| Current year financial effects | Additional impairment charges related to customers impacted by the Ditwah cyclonic and flood

disasters amounted to Rs. 1.2 Bn. (Note 18 – Impairment

charges/(reversal) and other losses ).

|

| Significant risk of material adjustments within the next annual reporting period (i.e. in 2026) |

The Group does not anticipate a significant risk of a material adjustment within the next

annual reporting period to the carrying amounts of assets and liabilities reported in the

Financial Statements. (Note 10.1 – Table 28 (e)) |

| Anticipated financial effects over short, medium and long term | Transitional Relief (Note 09 (d)) . |

| Climate resilience | Transitional Relief (Note 09 (e)) . |

| Significant judgements and uncertainties | Significant uncertainty stemming from data gaps directly affects the assessment of credit risk related to climate-induced physical risks. The lack of high-resolution, location-specific historical and projected climate data limits the ability to accurately evaluate how borrowers are exposed to physical hazards. Additionally, insufficient information on borrower-level climate vulnerability such as the resilience of their assets, infrastructure, and adaptive capacity hampers precise risk measurement. This makes it challenging to differentiate which borrowers or portfolios are most susceptible to physical damage, operational disruptions, or declines in asset value due to climate events. The Group's judgement that no material adjustment to the carrying amounts of assets and liabilities will be required in the next reporting period is subject to significant uncertainty given the risk that climate events could intensify more rapidly and abruptly than expected. (Note 10.1 – Table 28). (Note 09 (c) and (e)) |

Customer Education: Providing resources and guidance to borrowers on risk

management and disaster preparedness, helping them mitigate potential impacts and improve

repayment capacity.

Customer Education: Providing resources and guidance to borrowers on risk

management and disaster preparedness, helping them mitigate potential impacts and improve

repayment capacity.Transition risk to the loan portfolio from carbon intensive industries

Figure – 56

| Climate-related risk 02 | Transition risk refers to the financial risks arising from the economy’s shift toward a low-carbon and sustainable model, including changes in policies, regulations, market preferences, and technology adoption. |

| Description | In the context of Sri Lanka, a low-emission country with per capita GHG emissions of approximately 1.02 metric tons of CO₂e, transition risks are particularly relevant as emissions have been rising alongside economic growth. The country’s NDCs provide a framework to reduce emissions and guide the economy’s shift towards a sustainable, low-carbon model, which may impact borrowers in high-emitting sectors. Borrowers in carbon-intensive sectors face financial strain from policy and regulatory shifts, market transitions, and decarbonisation pressures, potentially increasing default risks. Export-oriented borrowers additionally confront regulatory barriers, including carbon border adjustment mechanisms (CBAM) and stricter emissions standards in key international markets. To manage credit risk while supporting customers’ transition, the Bank prioritises engaging with clients to facilitate decarbonisation, providing guidance and incentives for sustainable practices, and integrating transition pathways into lending strategies. |

| Physical risk/Transition risk | Transition risk |

| Time period | M, L (Note 07 – Table 27). |

| Current and anticipated effects of those CRROs on the Bank’s business model and value chain | Current Impact No material impacts in 2025 |

Anticipated Impact

|

Declining creditworthiness of carbon-intensive borrowers

Declining creditworthiness of carbon-intensive borrowers| Where it is impacted Credit Risk:

to climate-related transition risk .

Reputational Risk:

|

|

| How the Bank has responded or plans to respond to CRROs in Business Strategy and Decision Making | Credit Risk Direct Mitigation Actions:

Direct Mitigation Actions:

|

| How the Bank is resourcing, and plans to resource the activities | Financial commitments: Committed for Rs. 30 Mn. (equivalent to USD 100,000) for

the development of the Climate Transition Plan along with capacity building initiatives

Human Capital Development: Provide training across relevant teams on transition risk analysis to strengthen internal expertise. Technology Integration: Deploy carbon footprint tracking systems and scenario analysis tools to assess impacts of regulatory changes. Strategic Partnerships: Collaborate with initiatives such as PCAF and join industry decarbonisation alliances to align with global best practices. Governance: Establish Board-level oversight for transition risk through the BIRMC to ensure accountability and informed decision-making. |

| Progress of the plans and initiatives |

|

| Current year financial effects | No material impacts in 2025 |

| Significant risk of material adjustments within the next annual reporting period (i.e. in 2026) |

The Group does not anticipate a sudden or extraordinary shifts over Policy, regulatory, and market adjustments related to the low-carbon transition in 2026. Accordingly, the Group does not anticipate a significant risk of a material adjustment within the next annual reporting period to the carrying amounts of assets and liabilities reported in the Financial Statements. (Note 10.1 – Table 28 (e)). |

| Anticipated financial effects over short, medium and long term | Transitional Relief (Note 09 (d)). |

| Climate resilience | Transitional Relief (Note 09 (e)). |

| Significant judgements and uncertainties | The Group is of the view that there will not be sudden or disruptive changes to the policy,

regulatory, and market adjustments related to the low-carbon transition in 2026. This assessment

is based on the current trajectory of announced government policies, the phased nature of upcoming

regulations (e.g., EU Carbon Border Adjustment Mechanism), and the existing momentum within

markets. However, significant uncertainty surrounds the medium to long-term, over pace, stringency, and enforcement of government climate policies and regulations, which directly impacts credit risk through transition risk. Political shifts, economic pressures, or social factors may delay, weaken, or alter the implementation of low-carbon policies, creating unpredictable timelines for when transition-related risks materialise. (Note 10.1 – Table 28 (d) and (e) on page 44). |

Reputational risk from inadequate climate response

Figure – 57

| Climate-related risk 03 | Negative stakeholder sentiment: Reputational risk arises for the Bank, if it is seen as lagging in its climate and sustainability response. This transition risk may impact creditworthiness, capital access, and long-term strategic positioning of the Bank. |

| Description | Increased stakeholder concern or negative feedback poses a significant transition risk to the

Bank, as it reflects growing expectations from investors, customers, regulators, and the public

regarding climate action and sustainability. If the Bank is perceived as slow to respond to these demands, it may face reputational damage, loss of investor confidence, customer attrition, regulatory scrutiny, and challenges in attracting or retaining talent. These reactions can ultimately impact the Bank’s financial stability, increase its cost of capital, and constrain strategic growth, making stakeholder sentiment a key non-financial risk factor. |

| Physical risk/Transition risk | Transition risk |

| Time period | S, M, L (Note 07 – Table 27). |

| Current and anticipated effects of those CRROs on the Bank’s business model and value chain | Current Impact

|

| How the Bank has responded or plans to respond to CRROs in its Business Strategy and Decision Making | Reputational Risk Direct Mitigation Actions:

|

| How the Bank is resourcing, and plans to resource the activities | Human Capital Development: Provide training to Legal and Compliance teams on

greenwashing litigation to build internal capacity for identifying and managing reputational risks. Technology Integration: Implement an integrated ESG data platform to ensure consistency, accuracy, and transparency in sustainability disclosures. Governance: Implement a tiered escalation mechanism for timely resolution of misaligned incidents. |

| Progress of the plans and initiatives |

|

| Current year financial effects | No material impacts in 2025 |

| Significant risk of material adjustments within the next annual reporting period (i.e. in 2026) |

No significant risk of a material adjustment is expected within the next annual reporting period to the carrying amounts of assets and liabilities reported in the Financial Statements. (Note 10.1 – Table 28 (e)). |

| Anticipated financial effects over short, medium and long term | Transitional Relief (Note 09 (d)). |

| Climate resilience | Transitional Relief (Note 09 (e)). |

| Significant judgements and uncertainties | The Bank operates in an increasingly complex and divergent global regulatory environment. This evolving landscape creates inherent uncertainty, exposing the Bank to potential legal challenges and regulatory penalties. These risks may arise from interpretations of the Bank's public climate commitments, the precision of its stated targets, or the clarity of its external communications. Failure to adequately manage these expectations could result in financial penalties and reputational damage. Further, the financial impact of reputational damage is highly uncertain and indirect, making it difficult to quantify. It may materialise through harder-to-measure channels such as a higher cost of capital, loss of preferential financing, exclusion from ESG funds, or attrition of customers and employees, potentially leading to material financial impacts in the medium to long term. |

Sustainable finance opportunities

Figure – 58

| Climate-related opportunity 01 | New revenue and lending opportunities from climate-linked avenues. | ||||||

| Description | Sustainable finance enables lending and investment portfolios with environmental objectives such as carbon reduction, clean energy, and climate resilience. It also enhances the Bank’s appeal to socially conscious investors, supporting revenue growth and strengthening its reputation as a responsible financial institution. | ||||||

| Physical risk/Transition risk | Transition risk | ||||||

| Time period | S, M, L (Note 07 – Table 27). | ||||||

| Current and anticipated effects of those CRROs on the Bank’s business model and value chain | Current Impact

|

||||||

Anticipated Impact

|

|||||||

Where it is impacted

|

|||||||

| How the Bank has responded or plans to respond to CRROs in its Business Strategy and Decision Making | Product Innovations and targets

|

||||||

| How the Bank is resourcing, and plans to resource the activities | Human Capital Development: Conducting specialised training programs for credit

officers to Identify and

acquire new lending opportunities in the Sustainable finance space. Technology Integration: Invested in Climate Assessment for Financial Institutions (CAFI) tool to quantify, categorise and track the climate-related investments as well as GHG reduction impact of funded projects. Green Capital Mobilisation: Raised of Rs.15 Bn. through Green Bond in 2025 |

||||||

| Progress of the plans and initiatives |

|||||||

| Current year financial effects |

Basel III Compliant – Tier 2 Green Bonds of Rs. 15 Bn. This enhanced the Bank’s capital

adequacy ratio (total capital) and supported the expansion of green lending.

|

||||||

| Significant risk of material adjustments within the next annual report period (i.e. in 2026) | No significant risk of a material adjustment within the next annual reporting period to the carrying amounts of assets and liabilities reported in the Financial Statements. | ||||||

| Anticipated financial effects over short, medium and long term | Transitional Relief (Note 09 (d)). | ||||||

| Climate resilience | Transitional Relief (Note 09 (e)). | ||||||

| Significant judgements and uncertainties | The growth of the sustainable finance market depends on economic conditions, the speed of government Policies and regulatory developments, and competitive dynamics. Furthermore, the future regulatory environment remains uncertain. Insufficient government incentives, such as tax benefits or guarantees for green loans, and changes in Government Policies on climate-linked sectors could reduce borrower demand. Conversely, the introduction of sudden, stringent regulations may escalate compliance and reporting costs for the Bank’s green bonds and loan products. |

Metrics and targets

The metrics and targets include cross-industry metrics, industry-based metrics and climate-related targets set by the Bank.

1. Cross – industry metrics

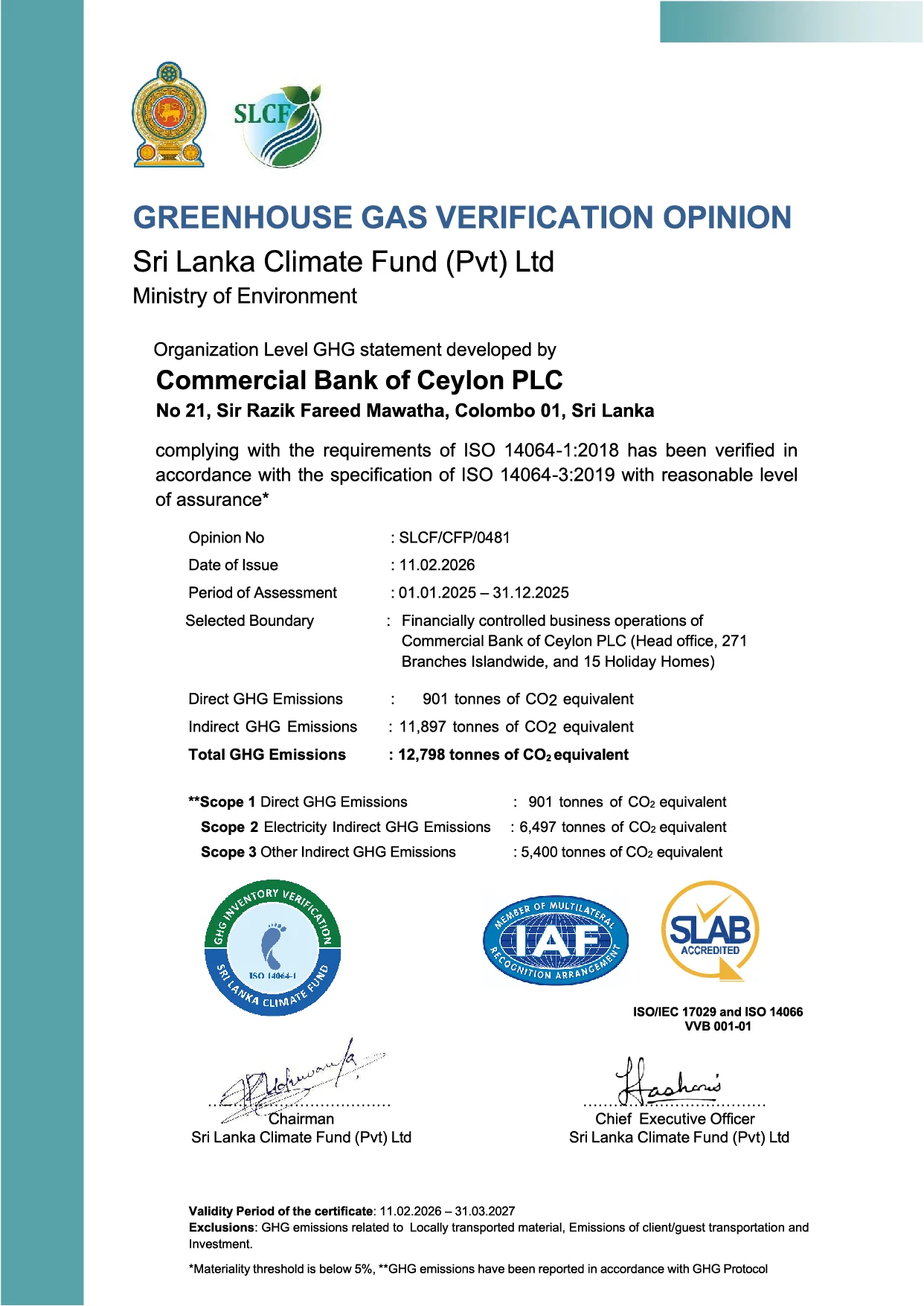

1.1 Greenhouse Gas (GHG) Emissions (SMT – 1.5)

The Bank measures and discloses its greenhouse gas (GHG) emissions in accordance with the GHG Protocol Corporate Standard, ISO 14064-1:2018, and SLFRS S2 requirements. It applies the financial control approach for GHG accounting, consistent with the consolidation principles used in its financial statements. This approach reflects the economic substance of the Bank’s relationships by accounting for all GHG emissions from operations over which the Bank has financial control.

GHG emissions are categorised into Scope 1, 2, and 3 emissions.

- Scope 1 (Direct Emissions): Emissions from owned or controlled sources, such as fuel combustion in company vehicles and backup generators.

- Scope 2 (Location-based Indirect Emissions): Emissions from purchased electricity, calculated using grid emission factors.

- Scope 3 (Other Indirect Emissions): All indirect greenhouse gas (GHG) emissions that occur in the value chain of the Bank but are not included in Scope 2.